The FCA calls this its first publication of this kind and states the document is not a set of predictions or regulatory guidance. It sets out plausible combinations of technologies and early signals of risk, grouped around three priorities: helping consumers, fighting financial crime, and supporting growth. FM Intelligence reads the scan as a signal of where supervisory attention is moving, not a rulebook.

The table below maps the report’s three themes to the questions each raises for compliance and risk functions.

|

FCA theme |

What the report describes |

Compliance watch-point |

|

Personalized intelligence |

AI agents become the main interface between consumers and firms, moving toward a “proxy economy” by 2030. |

Consent and accountability when an agent acts on a consumer’s behalf. |

|

Synthetic crime |

AI lowers the barrier to large-scale fraud and makes fabricated evidence harder to detect. |

Anomaly-based detection weakens as deepfake and APP exposure rises. |

|

Programmable finance |

Tokenization, stablecoins and smart contracts move from pilots to national strategies. |

Controls shift into code; reconciliation and concentration risk move rather than disappear. |

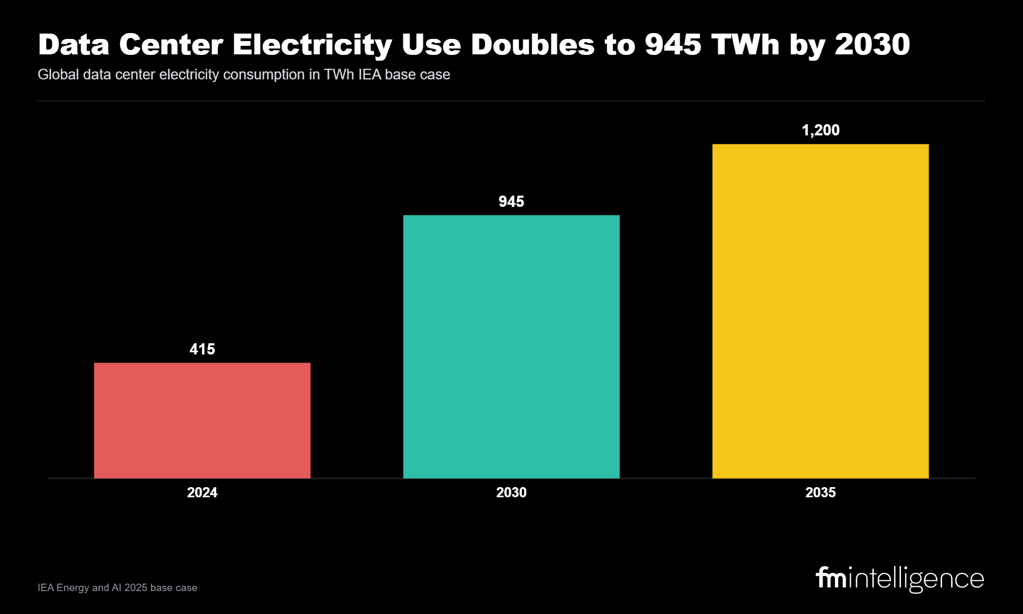

Data Center Electricity Doubles to 945 TWh by 2030

The scan opens with a “state of the world” section in which AI sits between competing pressures: energy, hardware, trade policy and trust. The hardest external number behind that framing comes from the International Energy Agency.

- Data center electricity use reached about 415 TWh in 2024, near 1.5% of global consumption, according to the IEA.

- The IEA base case projects this roughly doubles to about 945 TWh by 2030, close to Japan’s total electricity use today, and rises toward 1,200 TWh by 2035.

- The US and China account for nearly 80% of the projected increase, with AI-focused facilities driving most of the growth.

For operational-resilience teams, the relevance is concentration. The FCA flags the risk that many firms depend on the same handful of AI platforms and cloud providers, so a single shared vulnerability could reach multiple firms at once. Energy and hardware bottlenecks add a second layer, shaping where capacity, and therefore service continuity, actually sits.

Assistive, Advisory, Do-It-For-Me: Three Modes of Financial Delegation

The personalized intelligence chapter describes AI agents becoming the main interface between consumers and firms. The FCA sets out a progression of “escalating cognitive delegation” in three modes.

|

Mode |

What the agent does |

Control question |

|

Assistive |

Explains products, compares options, pre-fills forms and flags risks; the consumer still decides. |

Is disclosure reaching the consumer or only the agent? |

|

Advisory |

Recommends actions such as switching or refinancing; the consumer typically clicks through. |

Is a click-through informed consent? |

|

Do-it-for-me |

Acts within set limits: negotiates, transacts and reallocates, with periodic summaries only. |

Who is accountable for actions taken inside delegated authority? |

The report’s term for the end state is a “proxy economy”, in which the audience for a product is no longer the consumer but the agent that filters and acts for them. The FCA pairs the upside, including inclusion and scam avoidance, with named risks: opaque delegation, “sludge” practices that bias which options surface, and new “dark patterns” aimed at AI agents rather than people.

For compliance teams the questions are concrete:

- Is the firm serving the consumer or the consumer’s AI representative, and which one gives consent?

- Do agent-first channels still meet consumer-duty and disclosure obligations?

- Where do escalation-to-human points sit, and who owns the outcome when an agent acts within its limits?

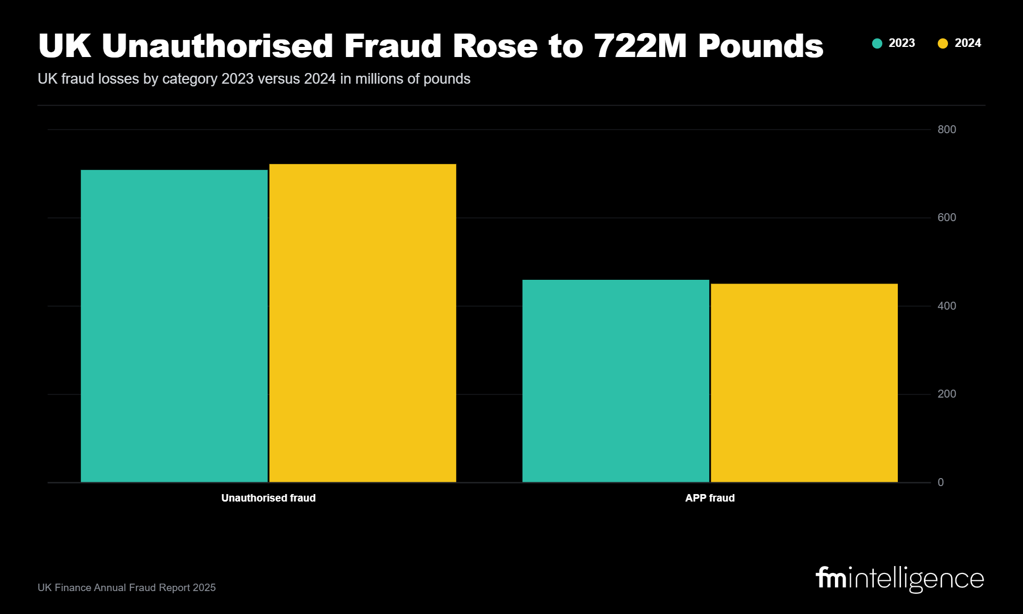

Synthetic Crime: From £1.17 Billion in UK Fraud to a $40 Billion Forecast

The report devotes the most space to synthetic crime: AI that lowers the barrier to large-scale fraud and makes fabricated evidence harder to detect. The current baseline is already large.

- UK fraud losses passed £1.17 billion in 2024, according to UK Finance. Unauthorized fraud accounted for £722 million across 3.13 million cases, up 2% year on year.

- Authorized push payment (APP) fraud fell 2% to £450.7 million, while APP case numbers dropped 20%.

- Investment fraud within APP rose 34% to £144.4 million, and banks prevented a further £1.45 billion of unauthorized fraud.

The forward risk is where the synthetic-crime framing concentrates.

- Deloitte’s Center for Financial Services estimates gen-AI-enabled fraud losses in the US could rise from $12.3 billion in 2023 to $40 billion by 2027, a 32% compound annual rate, with a conservative scenario near $22 billion.

- The FCA describes a shift from manipulating senses, through deepfake audio and video, to manipulating “sense-making”, including synthetic evidence trails built to pass both human and automated checks.

.png?width=1024)

The report also notes that frontier AI models have begun to demonstrate the ability to find previously unknown “zero-day” vulnerabilities across financial software, and points to cross-sector defensive collaboration as the counterweight. For financial-crime teams, the practical reading is that detection built on spotting anomalies may weaken when the tell becomes suspicious perfection rather than obvious error.

The Deloitte figure is a US-only projection covering gen-AI-enabled fraud broadly, not deepfakes alone, and the UK Finance totals predate the 2024 reimbursement-rule changes that reshaped APP incentives mid-year.

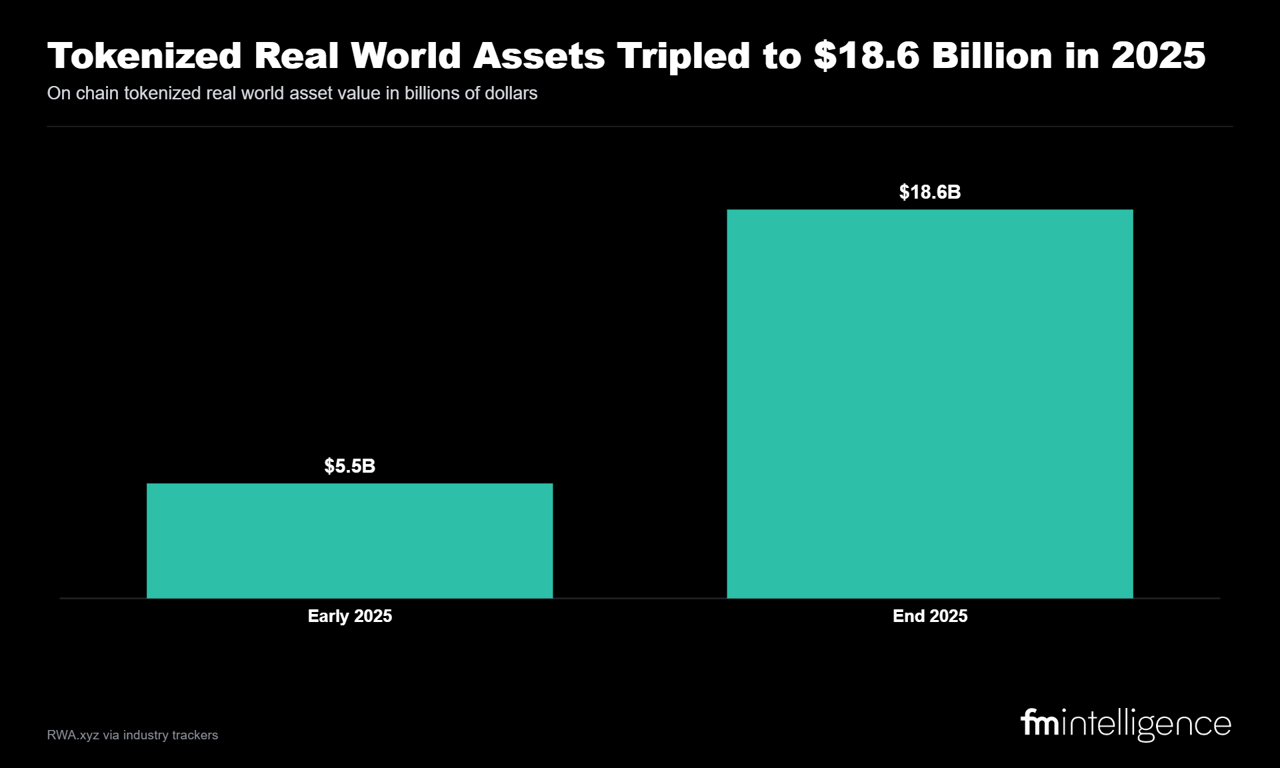

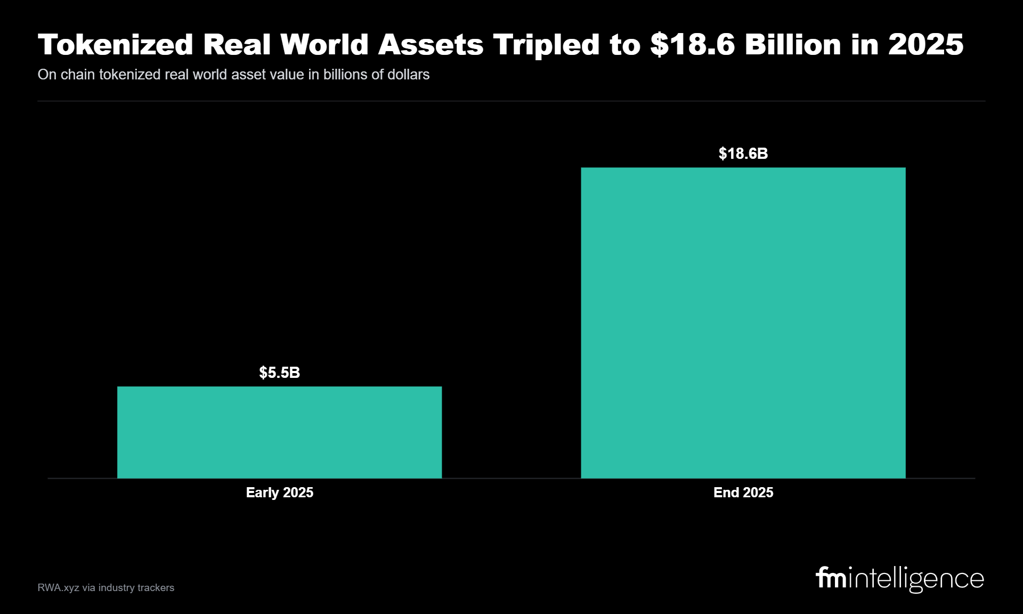

Programmable Finance: Tokenized Assets Tripled to $18.6 Billion in 2025

The final chapter covers DLT, tokenization, stablecoins, CBDCs and smart contracts moving from pilots to national strategies. The FCA frames the destination as “TradFi with protocol capabilities”, not a wholesale shift to DeFi.

- On-chain tokenized real-world assets rose from about $5.5 billion in early 2025 to roughly $18.6 billion by year-end, per RWA.xyz data cited across industry trackers, with analysts projecting growth toward $2 trillion by 2030.

- The stablecoin market cap reached an all-time high near $317 billion in early 2026, according to CoinDesk Data.

The report sets the UK’s “infrastructure-first” approach against two competing cross-border visions: the BIS Unified Ledger, a single integrated platform, and modular networks such as mBridge, sovereign ledgers linked by shared protocols. The FCA’s own Digital Securities Sandbox, run with the Bank of England, sits inside this direction.

For compliance teams, programmable settlement compresses the gap between instruction and execution. When a payment releases automatically on a data trigger, controls have to move upstream into code, and reconciliation risk shifts rather than disappears.

Disclaimer

Tokenization figures vary by tracker and methodology, so stablecoin and RWA totals from different sources are not directly comparable, and the 2030 projections are third-party estimates, not FCA or FM Intelligence forecasts.

This analysis summarizes the FCA Emerging Technology Horizon Scan 2026, published June 10, 2026, and pairs it with third-party market data. Fraud figures are from UK Finance (Annual Fraud Report 2025, covering 2024). Gen-AI fraud projections are from the Deloitte Center for Financial Services, on a 2023 base with a 2027 horizon for the US market. Data center electricity figures are IEA base-case projections. Tokenized-asset and stablecoin figures are drawn from industry trackers including RWA.xyz and CoinDesk Data and vary by methodology. All forward-looking numbers are attributed third-party estimates, not FM Intelligence projections, and should not be treated as forecasts. The FCA states its report is not a prediction or regulatory guidance.